Pradhan Mantri Shram Yogi Maan-Dhan Features and Eligibility Explained.

Pradhan Mantri Shram Yogi-Maan Dhan will be launched on 15th February, 2019. Lets know the features

The subscribers of this pension scheme will get an assured pension of Rs.3,000 from age 60.

Would you like to invest in shares (Stocks) with the help of RSI Technical Indicator easily, then click this link to know more.

Eligibility for Pradhan Mantri Shram Yogi Maan-Dhan pension Scheme…

The following category people are eligible for pension scheme…

- Monthly income should be less than or equal to Rs.15,000.

- Age must be between 18 years to 40 years.

- They should not be covered under the Employee Provident Fund Organisation (EPFO) or New Pension Scheme (NPS) or Employees State Insurance Corporation (ESIC) Scheme.

- They should not be income Taxpayers.

Their profession is like home-based workers, mid-day meal workers, head loaders, cobblers, rag pickers, domestic workers, washermen, rickshaw pullers, landless laborers, own account workers, agricultural workers, construction workers, beedi workers, handloom workers, leather workers, brick kiln workers audio-visual workers,

street vendors.

Pradhan Mantri Shram Yogi Maan-Dhan Features…

1. This Scheme is offering Minimum Pension…

The subscriber of this pension scheme will get a guaranteed pension of Rs.3,000 when they attain the age of 60 years.

2. Family Pension…

In case of the death of death of the subscriber after pension started, the spouse of the subscriber will be given 50% of the pension that

This family pension is applicable to spouse only.

If the subscriber dies much before the age of 60 and contributed regularly to the pension when he/she was alive, then spouse has the option to contribute to the pension scheme for remaining years.

Spouse can exit the scheme according to the Provisions of exit and withdrawals.

Government will contribute an equal portal to the Subscriber Contribution…

PM-SYM a voluntary pension scheme.

Where Government of India and the Subscriber will contribute 50:50 in this scheme.

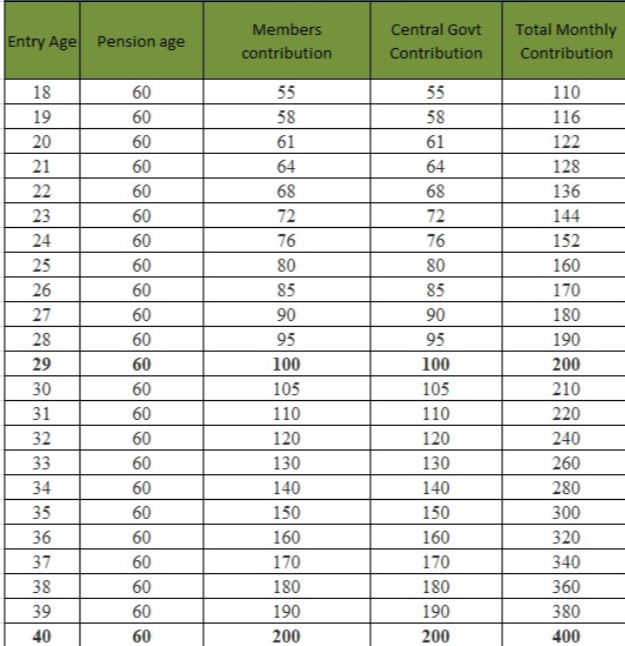

For example, a 29 years person has to contribute Rs.100 per month till he attains age of 60.

In addition, the Government will also contribute Rs.100 until the subscriber attains the age of 60.

4.Default Contributions…

If the subscribers failed to contribute regularly towards this scheme.

Then he/she will be allowed to regularize this scheme by paying all outstanding dues with interest or penalty described by the Government.

5. Pension Pay-Out…

Subscribers can join in this scheme if their age is between 18 to 40 years, after that they have to contribute money till they get age 60.

From age 60, subscribers will get a monthly pension of Rs.3,000 and family pension also provided in case of death of the Subscriber.

How much one should contribute in Pradhan Mantri Shram Yogi Maan-Dhan?…

The contribution for PM-SYM scheme should be done from SAvings Bank Account/Jana Dhan Account with auto debit facility till age 60.

The below table shows the amount of contribution for different ages.

Pradhan Mantri Shram Yogi Maan-Dhan Contribution Chart

www.paisahealth.in

How to enroll to Pradhan Mantri Shram Yogi Maan-Dhan?…

The subscriber should have mobile phone, Aadhar Number and Bank Account/Jana Dhan Account.

Eligible Subscribers can visit the CSC’S to enroll to PM-SYM using aadhar number and Bank Account/Jana Dhan Account on Self on Self-Certification basis.

Later, Subscribers can register them selves in PM-SYM portal or can download mobile app and can register using aadhar and Bank Account/Jana Dhan Account on Self-Certification basis.

Community Service Centers (CSC’S)will carry forward the enrollment process.

The workers can visit CSC’S along with Aadhar Card and Bank Account/Jana Dhana Account to get registered under this scheme.

Moreover, First month installment must be in the form of Cash.

In addition, A receipt will issued for the same.

All branches of LIC, the offices of EPFO/ESIC and all labour offices state and central Government will provide the un-organized workers this scheme.

All the benefits and procedure should be provided at the respective centers.

Who will be managing Pradhan Mantri Shram Yogi Maan-Dhan Fund?…

This scheme will be a Central Sector Scheme administered by the Ministry of Labour and Employment and implemented through Life Insurance Corporation of India and CSCs.

In addition, LIC will be the Pension Fund Manager and responsible for Pension

The amount collected under PM-SYM pension scheme shall be invested as per the investment pattern specified by the Government of India.

How to exit or withdraw from Pradhan Mantri Shram Yogi Maan-Dhan Scheme?…

- In case subscriber exits this scheme within a period of less than 10 years, the beneficiary’s share of contribution only will be returned to him with savings bank Account interest rate.

- If subscriber exits after a period of 10 years or more but before superannuation age.

- i.e. 60 years of age, the beneficiary’s share of contribution along with accumulated interest as actually earned by the fund or at the savings bank interest rate whichever is higher.

- If a beneficiary has given regular contributions and died due to any cause, then his/ her spouse will be entitled to continue the scheme subsequently by payment of regular contribution or exit by receiving the beneficiary’s contribution along with accumulated interest as actually earned by the fund or at the savings bank interest rate whichever is higher.

- If a beneficiary has given regular contributions and become permanently disabled due to any cause before the superannuation age.

- i.e. 60 years, and unable to continue to contribute under the scheme, his/ her spouse will be entitled to continue the scheme subsequently by payment of regular contribution or exit the scheme by receiving the beneficiary’s contribution with interest as actually earned by the fund or at the savings bank interest rate whichever is higher

- When the subscriber and spouse both die, the entire fund will be credited back to the Nominee.

- Any other exit provision, as may be decided by the Government on the advice of NSSB.

Pradhan Mantri Shram Yogi Maan-dhan – Is it worth for you?…

If a 18 year old person subscribed to this pension scheme, then he will get monthly pension of Rs.3,000 per month after 42 years

In addition, if you discount this Rs.3,000 with 6% inflation for 42 years, then that Rs.3,000 will be equal to Rs.259 in today’s cost.

But how many people can survive today with just Rs.259 per month.

Hence, this scheme just a election magic.

Instead, the Government should have tried adding more benefits to the NPS or Atal Pension Yojana.

Moreover, the monthly pension or Rs.3,000 will not increase after age 60 in this scheme, But the inflation will not stop increasing after the inflation.

Any how, it is up to every individual whether to consider this scheme or not.

But, the truth is this scheme is ignoring impact of inflation.

Moreover, We should not forget impact of inflation while planning financial goals like retirement.

Finally, this scheme is a waste Product to consider for your retirement. What’s your opinion?

Read the article about Budget 2019 changes and highlights… Click here to read.