Life Insurance Agents are making better profit than you How?

Life insurance agents used to sell most of us insurance policies to get profit for their livelihood.

But agents will try to push some policies to us.

Endowment types of policies are also heavily pushed by agents for us to buy.

Here, in this article, I am trying to tell you how much profit you will get and, at the same time, how much your agent is getting.

But many policyholders are arguing with me that their agents have given them back the commission that they are getting.

Hence they are dreaming that they are smart and made a huge profit in doing so.

Here, I will tell you whether these policyholders made a profit by taking commission back or not.

What is Life Insurance AGent Commission Pass Back?…

A typical life insurance agent will get a 35% 1st-year commission on the premium that you pay.

In addition, your agent will get a 5% commission on the premium that you will pay from 2nd year onwards till your policy matures. (It may vary a little from company to company).

But you people (policyholders) will demand some portion of the commission to be paid back.

As a result of this, these agents are paying back the commission that they are getting to the policyholders.

Here, these policyholders are thinking they have done a wise thing and made a huge profit by getting a passback of commission from the agents.

Moreover, policyholders will tell me that they not only got a passback of 1st-year commission; they also made agents pay a major part of the 1st-year premium from the agent’s pocket.

Please do not tell me silly answers that you need agent service for premium paying and in case of death.

Here, in this article, I will try to tell whether the policyholders really got benefitted by getting passback of premium (commission) from the life insurance agent.

In addition, different agents will get different profits as they give different amounts as a passback of commission.

As a result of this, their return “%” will vary.

Now, let’s see different scenarios as shown below.

Scenario 1: How much is the return that the life insurance agent will make? ..

Some life insurance agents will give a passback of their 1st-year commission as a passback to the policyholder.

Let’s assume that you opted for a life insurance policy with a 20-year premium-paying term, and the premium is Rs. 1,00,000 per year.

In the above case, the agent actually will get Rs. 35,000 as 1st-year commission.

If the agent gives this Rs. 35,000 back to you, let’s calculate how much return he makes after giving this Rs. 35,000 as a passback.

If you see the above image, I have taken cash flow of Rs. 5,000.

Here, I have assumed that the agent has given back to you Rs. 35,000 that he gets on the 1st-year premium.

In addition, the agent has spent only Rs. 5,000 from his pocket.

But the agent has given away Rs. 35,000 (1st-year commission) only, which is not from the agent’s pocket.

I.e., Rs. 5,000 from his pocket and took Rs. 35,000 from your premium payment as commission, and this commission of Rs. 35,000 he passed back to you.

So, this Rs. 35,000 we cannot consider as an expenditure for the life insurance agent for calculating his return from your life insurance premium payment.

As a result of this, I cannot enter that Rs. 35,000 cash flow for calculation purposes.

In addition, I have also assumed that the agent has spent Rs. 5,000 travelling a few times to meet and to complete the policy proceedings.

If you see at the bottom of the above image, it is very clearly visible that age got a return of 99% return on investment.

So, after seeing the above return of life insurance agents, it looks like life insurance agents are looting from you.

But a few people (policyholders) may argue with me that they will get Rs. 50,000 as the pass of commission from life insurance agents.

So, let’s calculate returns for that scenario also.

Scenario 2: How much is the return of the life insurance agent?

In this scenario, I am assuming that the agent has given the pass back 50% (Rs. 50,000) to the policyholder and spent Rs. 5,000 for travelling, etc. to complete this policy.

Here, the agent has spent only Rs. 20,000 from his pocket (Rs. 15,000 towards premium + Rs. 5,000 as completing the policy).

Now, let’s calculate the agent’s return in this scenario.

If you see the above image, the return on investment for the life insurance agent is 24.677%.

Again, the above return is also quite good for the agent.

Scenario 3: How much return does that life insurance agent get? …

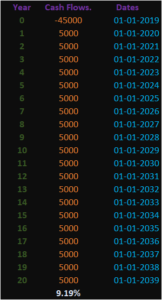

Let’s assume in the scenario that the agent gives back Rs. 45,000 (Rs. 5,000 as expenses + Rs. 40,000 from his pocket) to the policyholder.

Hence Out of the Rs. 1,00,000 premium, Rs. 75,000 will be paid by the agent and Rs. 25,000 will be paid by the policyholder.

But for calculating the return, we will take R. 45,000 only. You can see this Rs. 45,000 entry in the below image.

If you see the above image, the life insurance agent got a 9.19% return from the policy you took.

So, after seeing all three scenarios above, we found that the life insurance agent got a return of 99%, 24%, and 9.19%, respectively, in different scenarios.

In addition, for the policyholders, it is not important to know how much return the agent is getting.

How much return are you (the policyholder) getting from the endowment-type life insurance policies? …

It is very important for the policyholders to know how much return they are getting for themselves.

I have written an article about Lic Jeevan Anand return, which is an endowment policy.

In addition, after reading Jeevan Anand’s article, you will understand that the return that policyholders will get from endowment-type life insurance policies is around 4 to 6% only.

I have written an article about why you should not invest in ULIP of life insurance companies only because maturity is tax-free.

Why had I stopped selling life insurance policies 8 years ago? …

When I stopped selling life insurance policies 8 years ago, few people suspected that I had started a new business, which gives me more profit.

But that is not the case. If you read the entire article, you may have understood that policyholders are not getting enough returns, which can beat inflation.

In addition, if you do not take care of inflation, One day it will make you poor.

Here, you may argue that everyone needs life insurance to safeguard dependents.

Yes, I do agree that you may need life insurance But to protect dependents, Term Life Insurance is the best option.

In addition, this term life insurance also should be taken under need-based analysis only.

Moreover, watch this video to understand need-based analysis for life insurance.

But the language spoken in the video is Telugu.

Conclusion…

By taking a commission as a passback from the life insurance agent, do not dream that you have done a wise thing.

As you are considering the impact of inflation, your money is actually not growing (maintaining its purchasing power).

In fact, you are becoming poorer day by day.

Hence, I suggest you not take these kinds of endowment types of policies and try to take term life insurance under need-based analysis only.

Read Why life insurance will become poor in India. …

Also read about One Core term insurance: Why you should not take?

and read about how much life insurance is needed for you.?

Also read about is FD a good investment?

And read about human life value in life insurance.

Also read Why life insurance and savings should not be mixed?…