Poor – Why Life Insurance Agents will become in India ?

Life Insurance Agents in India will become Poor.

Don’t you believe me, then read this entire article to understand why?

Just before I have stopped my career as Life Insurance Agent 8 years back in LIC Of India, I had seen a hoarding at a famous junction in my City.

Hoarding had the following Catchy Head Line.

” Become a Lic Agent” to earn income in lakhs“.

In addition, The Hoarding stated that the retired employees, housewives, teachers, and fresh graduates, etc can become a part/full-time Lic Agents to earn huge money as per their need.

Moreover, That Hoarding was kept by a Development Officer of Lic of India, Kakinada, Andhra Pradesh.

However, This Hoarding belongs to a Development Office of Lic Of India.

In addition, He is looking to recruit new Lic Agents.

Here, in the title, I am saying that Life Insurance Agents will become poor. But most people are looking to become Insurance Agents.

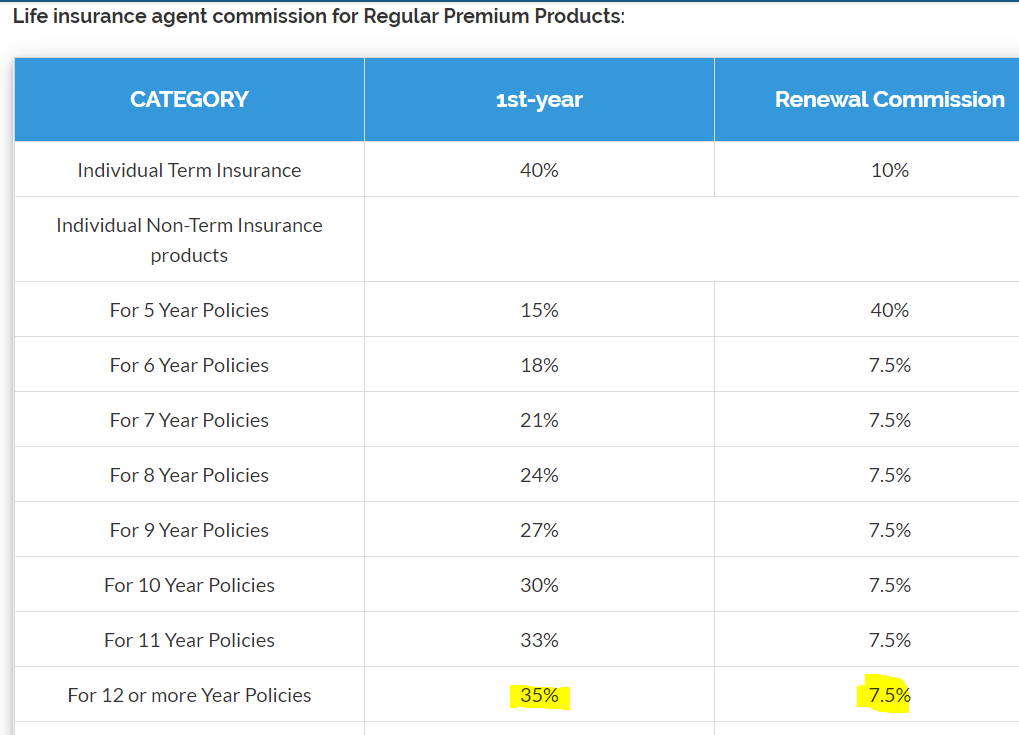

But before that, You should know that what is commission (income) structure for a Life Insurance Agent…

If you find the above image, You can find that the agent can earn a high commission if the premium paying term is more than 12 years.

But the renewal commission of 7.5% may not be paid for every year till premium paying term for the agents.

In addition, the insurance company most cases will pay 35% as commission for the first year and 5% from the second year onwards till premiums paid as commission to agents in Life Insurance.

Moreover, I am talking about Endowment type policies for this analysis.

Here, I took the above image from the following Finbucket website.

Why Insurance agent will become Poor?

After seeing the commission structure for the agents, You may be thinking that I am lying.

But I will prove that the agents will become poor if want to become insurance agents, especially Life Insurance Agents.

Here, Insurance agents in India can not get quality policies ( high premium policies) without giving back commission to policyholders.

Let’s say that the policyholder has to pay 1 lakh premium per annum.

Then the agent will get Rs.35,000 as commission for the 1st year.

But most agents will not take 1 lakh cheque from the client.

Instead, they will take a cheque for a lower amount, and the balance amount agents will pay from their pocket.

and agents will give a receipt for a full 1 lakh amount to the policyholder.

In addition, this entire process of giving back commission to the policyholder is simply called as ” Pass Back of Commission”.

In the process, agents sometimes will give a higher amount as pass back and becoming poor.

To understand it better, we should discuss different scenarios…

Please do read all the scenarios to understand.

Scenario 1) Why agents will become Poor?…

If you see the above image, I have assumed that the PolicyHolder is paying 1 lakh per annum.

In addition, the policyholder will pay a premium for 21 years.

Here, In this scenario Agent has spent Rs.5,000 for completing this policy.

And the agent gave pass back of Rs.35,000 to the policyholder.

I.e Agent’s 1st-year commission only.

In spite of giving 1st-year commission as pass back, the agent’s return is 99%.

But the story is not ended here.

Most of the times’ agents have to give more money as pass back than we have assumed above.

Imp Note: – As 1st-year commission just came into agents’ pocket and went out as pass to the policyholder, it should not be entered as cash flow for calculating returns.

Scenario 2) Why agents will not become rich?…

As shown in the above image, If the agent gives Rs.20,000 extra than the 1st-year commission that he receives,

then the return on investment for the agent still 24.67%.

Which is also a good return on investment for the agent.

Again, the story is not ended here.

Let’s see one more scenario.

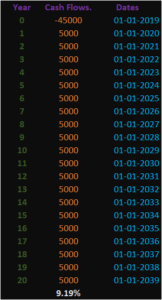

Scenario 3) Why agents will become Poor?…

As shown in the image, the agent is getting a return on investment of 9.19%.

In spite of giving pass back of Rs.45,000 extra than the 1st year commission ( Rs.35,000 + Rs.45,000).

Again, the scenarios not over.

Let’s look at one more scenario.

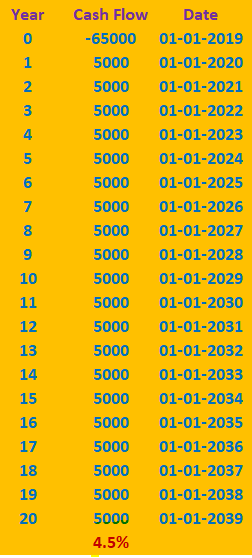

Scenario 4) Why agents will become Poor?…

Some of you may feel that a Life Insurance agent may not give more pass back which is shown in the above image.

But I have seen and heard stories that so many agents are giving pass back of entire 1st- year premium to the policyholder.

You can find In the above example, The Life Insurance Agent got only a 4.5% return on his investment.

In addition, I have assumed in the above example that the agent has paid an entire 1st-year premium as commission.

Moreover, the return on investment for the agent in this scenario is far below the Bank Fd interest rate at present.

Few More Important Points Why Insurance Agents will become Poor?…

Here, I will tell you why one should not become an insurance agent?

- In scenario 4) It is very clear that the return on investment is just 4.5% for the agent.

- In addition, it is just below or around the inflation rate only.

- But few agents will argue with me that they will get some benefits because of Club MemberShip.

- To avail those benefits, agents have to bring a certain amount of premium every year.

- But buying Horse for the reason that you found Horse Girth on the road is not a wise idea.

- In Scenario 3) it is visible that the return on investment is 9%.

- Which definitely over and above present Bank Interest rate and Inflation Rate.

- Similarly, In Scenario 2) and Scenario 1) the return is 24% and 99% respectively.

- Here, the above 3 Scenarios are looking fine. Isn’t it?

- But it is not.

- I will tellYou why?

- Let’s Assume that You are a retired employee and would like to give the pass back of 1st-year entire premium or part to the policyholder.

- If your retirement kitty got over 1st year itself for giving pass backs, then you have to take a loan to give pass backs from the 2nd year onwards.

- But your return will be minimized because of the interest that you have to pay on the loans.

- In the case of the agents who started with zero funds in the pocket, this situation will be much worse.

- Moreover, this pass back of commission is a never-ending story and the agent has to give this pass back every year to get new policies.

- Here, the agents are dreaming that they will get surely renewal commission once they stop doing insurance business.

- But IRDA is recently planning to stop giving commission for the orphaned policies.

- Orphan policies are those for which policyholders are paying renewal premiums without the agent’s intervention.

- You can read this article to know more.

- However, the agents who have completed at least 5 years as an agent may not be affected by orphaned policies rule as of now.

- But regulation can change at any time.

- An example is that the Government removed the defined pension system for the Govt Employees.

A few other Points to Discuss are…

Some Agents are telling me that they would like to do policies for the poor only.

As they do know these pass backs of commission or premiums.

But the truth is in recent times Govt started Jan Dhan Yojana accounts and started giving life insurance coverage for 2 lakh for a premium of Rs.330 per annum.

As a result of this poor people started surrendering their existing endowment life insurance policies.

But if you want to do policies for educated and for rich, then one has to give pass back of premium or commission.

Sometimes this pass back of premium will be as high as a full 1st-year premium as I told above.

My opinion…

Some Agents may argue that they will give only 1st-year commission only as pass back, not the premium.

In addition, they are giving 1st-year commission as pass back means there is no loss to their pocket.

But remember, the full-time agent is doing this insurance business for his livelihood.

If the agent is not getting any income by the way of commission means, he has to take a loan for his livelihood.

In the case of part-time agents like retired teachers, housewives, Pvt employees, and business people, they will feel that they have funds for the livelihood and hence there will be no loss.

But remember, even these people spent their valuable time in order to get new policies and to serve these policies.

In addition, all of us know that “Time is Money”.

So, spending valuable time on an unpredicted future for these part-time agents also not a good idea.

The future is not in your hand, policyholders can die any time, can surrender policy any time and can stop paying premium any time.

In addition, the regulator (IRDAI) can change the rules about the renewal commission.

Moreover, there are a lot of if’s and but’s in giving pass backs to the policyholder.

When there are a lot of if’s and but’s means that business is not good to do.

This situation is not only for Life Insurance agents but also for health insurance( general insurance) agents.

In addition, You are giving pass back of premium from your pocket to the policyholder means that you are investing money to get a profit.

So, You are doing business.

I have recently written an article about the best way to do business.

Click this link to read the article.

A good business always should give an extra 10% to 15% return over and above inflation.

If a Business which is not giving enough return over and inflation, then you will become poor one day by doing that business.

In addition, Frankly Speaking, If you give pass back like in Scenario 1) also, Agents’ return on investment will not be enough to beat inflation in a big way.

As other factors like pass back needed every year, regulation, client mindset change, client death, and client surrendering policies, etc.

So, investing in equity mutual funds, real estate, etc depending on risk tolerance and financial situation is better instead of doing pass back agent business.

In addition, you can do another low-risk business-like Juice Shop, Milk Dairy, Pan Shop, and a small Tiffin Hotel, etc.

Where your return on investment, you can easily assess every day and every month.

Unlike in Pass Back of Commission and Premium Insurance Agency Business in India.

What is the solution for the agents?

The Development Officers of Life Insurance Companies always try to misguide you.

Watch this video to know how they will misguide you?…

I strongly advise part-time agents like retired employees etc not to give any kind of pass back of commission or premium to the policyholder.

In addition, if you are not able to get any kind of policies without giving any pass back, then it is better to quit your agency.

Moreover, It is wise to do the safest business like a small Kirana and pan shop kind of business where your profit is certain.

Whereas income in insurance agency business very uncertain.

When it comes to full-time insurance agents in India, I strongly recommend you also not to do business by giving pass backs.

In addition, Do not fall in Development Officer’s traps and Club Member Ship traps.

Moreover, You will only make development officers rich by giving pass backs.

Always try to give the right policies for the right people.

Regulators in India are there to do good for the people not for the intermediaries’ benefit.

So, it is wise to improve your skills in order to serve or advise your customers in a proper way.

In addition, try to complete professional Certifications Like “CFP” etc, and also try to become Sebi Registered Investment Adviser.

In the process, you will be rewarded too by your customers.

Read this article How Life Insurance Agents are earning more than the policyholder?

Also, read the article that Why you should not invest in ULIPs for tax-free reasons?

Read article about the usage of time value money in your life.

Also read article about Tithe – Why it is bad?

Read Lic Bima Jyothi Plan.