Navjeevan Plan No.853 of Lic-Features and Review

LIC of India launched a new Non-Linked with profit Plan i.e Navjeevan Plan No.853 on 18th March 2019. Let us discuss it’s features and review.

Why LIC of India launch new Plans in Jan to March Months every year?…

If you see the history, LIC always launches new policies every year in January to march.

Here, The reason is simple Employees or Tax Payers usually plan their tax-saving investments from January to March months.

So, in order to attract these taxpayers, LIC of India launches new plans every year in Jan to March months.

Navjeevan Plan No.853 Features and Eligibility…

As I said above, this Navjeevan Plan No.853 is non-linked with profit policy.

In addition, The premium can be paid either as a single premium ( as a lump sum) or for a limited period i.e for 5 years.

There are some other features for this plan…

- you can buy this plan both online and offline.

- If you buy this policy online you will get a discount of 2% in case of a single premium and in case a limited period payment of premium 5% discount for a period of 5 years.

- In the case of Limited Premium payment option, you can pay premiums yearly or Half Yearly or Quarterly or Monthly

- Paid-up benefit is available when the premiums are paid for two years.

- You can surrender your policy at any point if the premium paid is single. But in case of a limited premium option, you can surrender the policy after two years of completion of the policy term.

- You can get a loan from this policy. In the case of Single premium, you can get a loan after 3 months and the max loan amount is 80% of the surrender value.

- If the Premiums are paid for two years, then the Loan facility is available in the Limited Premium Payment plan.

- The max loan can be taken is 80% of surrender value ( for in-force policies) and 70% in case of paid-up policies.

- * If your age is less than 8 years, then the commencement of risk (insurance coverage) will be started either one day before the completion of 2 years from the date of commencement of policy or one day before the policy anniversary coinciding immediately following the completion of 8 years of age whichever is earlier.

- * This plan is offering Accidental Rider and the rider like settlement option rider (both in case of maturity and death benefit)

What is Option 1 and Option 2 in Navjeevan Plan No.853 of LIC?

This option 1 and Option 2 are applicable only when if you pay a premium as limited payment not when you have paid a premium as a Lump sum.

When the premium is paid as a single premium than the death benefit 10 times of the single premium paid.

But when you have paid premium as Limited premium payment, then the following benefits are there…

- If you are is less then 45 years, then you will receive 10 times of annual premium payment as a death benefit.

- If your age is above 45 years, then you chose one out of two options available.

- Option 1) You can choose the option of 10 times of annualized premium as a death benefit or

- option 2) You can choose the option of 7 times of annualized premium as a death benefit.

What are the Benefits under Navjeevan Plan No.853 of Lic?…

Below benefits are the maturity and death benefits of this plan…

What is the Maturity Benefit under Navjeevan Plan No.853 of LIC?…

In case the policyholder of this plan survives till the policy term then he will receive Basic Sum Assured + Loyalty Addition as Maturity Benefit.

What is the death benefit under the Navjeevan Plan No.853 of LIC?…

- If the policyholder dies before completion of the first 5 years, and before the commencement of risk ( Insurance coverage), then premiums will be refunded without any interest.

- But in case of death of policyholder before completion of 5 years, but after the commencement of risk ( insurance coverage), then the nominee will receive Sum Assured as Death Benefit.

- If the death of Policyholder occurs after completion of 5 policy years, and before the maturity then the nominee will receive Sum Assured + Loyalty Additions as Death Benefit.

Sum Assured meaning in case of Death Benefit?..

- In case of death, The highest of the below options will be paid as death benefit.

1.Basic Sum Assured

2. 10 Times of Single premium

- In the case of Limited Premium Payment option, higher of the below options will be paid as a death benefit…

- Basic Sum Assured.

- 10 times of annual premium ( in case of option 1 is selected).or

- and 7 times of annual premium ( in case of option 2 is selected).

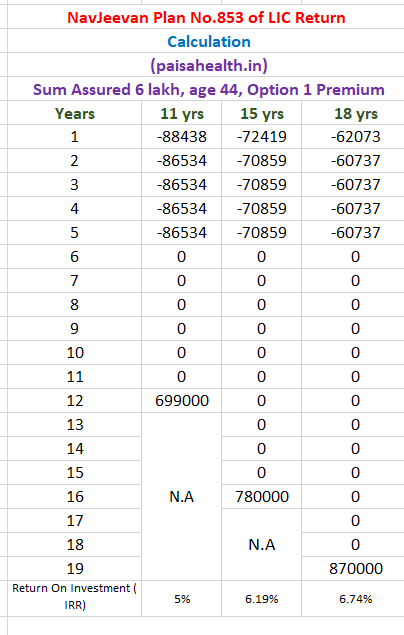

Navjeevan Plan No.853 Return on Investment Calculation…

Imp Note:- The Loyalty Addition assumed for 11 years is Rs.150, for 15 yrs Rs.200 and for 18 yrs Rs.250, and the premium is a yearly premium.

The 2nd year premium will be slightly lower as GST Rate will be lower from 2nd year onwards for Life Insurance premiums.

The source for Premium rates is https://www.insurance21.in/premium-calculator/lic-navjeevan-853.html

Navjeevan Plan No.853 Review and Should you invest in it?…

- Frankly speaking, LIC Of India launched this plan to lure people in the month of March 2019 who look for policies to buy for tax saving.

- But you should not buy a life insurance policy not only for tax saving.

- Your main priority should be while buying life insurance to have proper life insurance coverage to protect your dependents and Financial Goals in case of your sudden demise.

- As this plan provides low insurance coverage, it is not sufficient for protecting your financial needs.

- Most Planners like me suggest Need-Based Analysis to take life Insurance.

- If you are not eligible for enough life insurance coverage under need-based analysis, then at least you should take a life insurance policy to cover at least 10 to 15 times of your annual income.

- Not only this you should not mix your life insurance with Investment. Read this article why?

- Moreover, If you see the return expected from this policy in the above table image.

- You can see the return is around 5% to 7% only.

- But when you are investing for such long periods, you should not be investing in such low returns.

- Finally, This Navjeevan Plan No.853 of LIC OF INDIA Neither good for Life Insurance Coverage nor for Investment purposes.

- So, It’s up to you to invest in this plan or not…

- According to my view taking term life insurance under need-based analysis is good to protect dependents from a financial loss in case of your sudden demise.

- In addition, investing the rest of money in Financial Assets is a good option.

- You can consider investing in mutual funds, Bank FD, PPF, etc.

- However, investing goal-oriented and following asset allocation and risk tolerance is Good.

- What is your opinion?

Read article About Ulips- Why you should not buy even they are tax fee at maturity. Click here the read it.