CII – What it is? and How to calculate tax with it?

CII full form is the Cost Inflation Index. We can calculate the capital gain tax on real estate, gold, and debt mutual fund with CII.

can you guess these numbers 100,105,109?

Here, I am not asking you to do any calculations.

The above numbers belong to the CII table.

In addition, the above numbers belong to the Cost Inflation Index for the financial year 2001-2002, 2002-2003, and 2003-2004 respectively.

Moreover, When you sell, these numbers will help you in not paying higher taxes on your real estate, gold, and debt mutual funds,

Now, Let’s learn that How we can save tax with this table?

What is CII?

Let’s assume that you had bought a house worth 2 cr in 2002.

In addition, let’s assume that the price of the house increased to 3 cr till 2010.

If you sell that house now, then you may need to pay a huge chunk of tax on the total 1 cr ( Sale Price 3cr – Purchase Price 2 cr ) gain that you received.

In order to prevent you from paying higher taxes, Cost Index will be used.

Your purchase price of the asset will be indexed with the help of the CII.

In other words, it will be revalued or increased from its original price.

So that the impact of inflation will be deducted from the gain or profit you received from the sale of the Capital Asset.

As a result of this, you will end up paying lower taxes on the sale of the Capital Asset.

But How? I will tell you later. let’s understand further.

Why Capital Gain Tax is calculated using CII?

CII will be used for Capital Assets like gold, real estate, debt mutual funds or debentures to calculated tax.

Asset Class prices will increase due to inflation over a period of time.

In addition, due to inflation, the Purchasing power of money will be eroded.

However, We keep cost price when we sell the Capital Asset ( Sale Price – Purchasing Price) despite the increasing inflation.

I.e like 3 cr Sale Price – 2 cr Purchasing price, an example which I told above.

So, if you simply deduct the cost price (Purchase price) from the sale price, you have to pay a higher tax due to this method.

When Do You need to pay tax actually?

You know that we have to taxes when we get a profit only on the investment made after all the expenses.

In addition, we have to apply the same formulae for real estate, gold, and debt mutual funds investment.

Moreover, we have to deduct the inflation from the profit that you received.

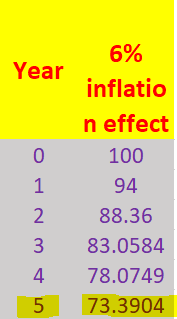

Let’s understand the impact of inflation on the money.

Let’s say You have Rs.100 in your hand today.

In addition, You kept this Rs.100 at your home without investing for 5 years.

At the same there a Cricket ball available in the market and its cost is Rs.100 today.

Now, after 5 years you went to the market to buy a cricket ball.

But you can not buy a cricket ball with this Rs.100.

The reason for this is because due to inflation, the cost of the ball is not equal to Rs.100 that you have in your hand.

In addition, the cost of the ball after 5 years is Rs.133( if the inflation rate is 6%).

In other words, Rs.100 value is equal to Rs.73 only and not equal to Rs.100 ( even though Rs.100 is printed on the note).

You have to pay tax after deducting inflation…

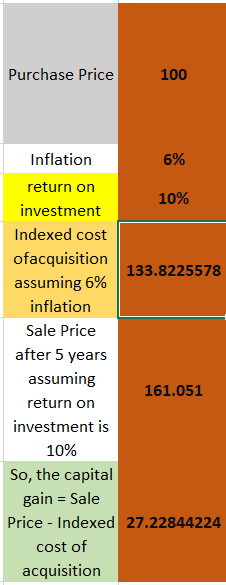

Again, if you have invested Rs.100 and got a return on investment of 6% per annum.

Then today’s Rs.100 will become Rs.133 after 5 years ( assuming 6% return on the investment).

Moreover, Rs.100 has maintained it’s purchasing power ( i.e you were able to buy the ball today and also after 5 years).

But if you got a return of 10% return on Rs.100 investment, then you got a profit of an extra 4% after deducting a 6% inflation impact.

In addition, You need to pay some tax on this 4% extra profit that you received over and above inflation impact.

In the above image, the capital gain is Rs.161 (Sale Price ) – 133 ( Indexed cost of Purchase price ) = 27 ( Real Gain).

In addition, I have assumed that Rs.100 is invested for 5 years.

Moreover, 10% is the return on investment and the country’s inflation in the same period is 6%

Similarly, While calculating the profit on your investments in real estate, gold, and debt mutual funds, the same concept

which I have explained above will be applied using the CII table.

In addition, CII table you in determining the country’s inflation effect on your asset.

you need to pay tax If the sale price – Cost Price ( Purchase price after country’s inflation effect) is a + number,

In addition, if this number negative number or neutral ( no profit or no loss),

then no need of paying any tax.

However, this CII concept is not applicable to investments made in Bank Fixed deposits.

So, CII will help you in determining the real gain.

I.e Real Gain = Sale price of the Asset – Inflation adjusted Purchase price of the asset.

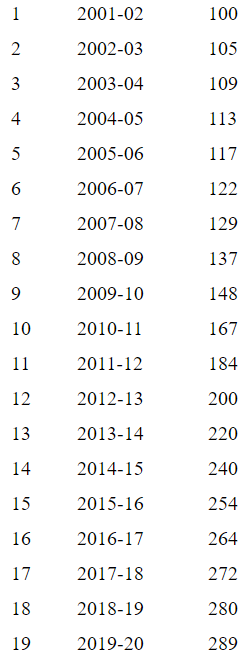

How the Cost Inflation Index values are calculated?

Till now, we learned that the LTCG will be paid only after deducting the inflation effect from the sale price.

But each person will be having a different view on inflation.

Hence, the CBDT ( Central Board of Direct taxes ) has introduced a unique number based method to calculate the capital gain tax.

In addition, CBDT will announce the inflation index figures every financial year to calculate the indexed cost of acquisition of the capital asset.

Cost Inflation Index = 75% of the avg rise in the consumer price index ( urban) * for the immediately preceding year.

Here, CII compares the current price of the basket of goods and services ( which represent the economy) with the price of the basket of goods and services in the previous financial year to calculate an increase in prices.

How the CII is calculated is not important for us.

What is the Base Year Concept in Cost Inflation Index?…

The Government has defined the base year for CII as 2001-2002.

In addition, 100 is the factor for all the purchased made before 2001.

The purchase price will be higher of the below two in case of taxpayer bought the capital asset before the base year of the CII 2001.

i.e Actual Cost or Fair Market Value ( FMV) as on 1st day of the base year.

Here, the Indexation benefit will be applied to the purchased price that arrived (calculated) from the above formulae.

In addition, the FMV value will be arrived based on the registered Valuer’s report.

Why the Govt has shifted base year from 1981-82 to 2001-2002?…

Earlier, The base year for the CII was 1981-82.

but the taxpayers were finding it difficult to find values for the properties bought before 1st, April 1981.

In addition, tax authorities also finding difficult to rely on the valuation reports.

As a result of this, the Govt has shifted the base year from 1981-82 to 2001-2002.

So that valuations can be calculated quickly and accurately.

Cost Inflation Index

Applicability of Cost Inflation Index in Capital Gain Calculation…

CII is used to calculate the Long Term Capital Gain in gold, debt mutual funds, etc securities, and real estate investment.

LTCG is flat 10% ( above the gain of 1 lakh ) after 1 year in equity.

So, CII usage in equity investment is impossible.

But in case of debt mutual funds and fixed maturity plans, it can be used to calculate LTCG.

Real Estate Investment…

If the real estate investment if your holding period is more than 2 years, then we can calculate LTCG for it.

How to Calculate LTCG in Debt Mutual Funds…

We can Calculate Long Term Capital Gain in Debt Funds if the units were held more than 3 years.

How CII is applied to calculate LTCG?…

When CII is applied to the Purchase price ( Cost of acquisition) of the asset,

then it becomes the “ Indexed cost of the acquisition“.

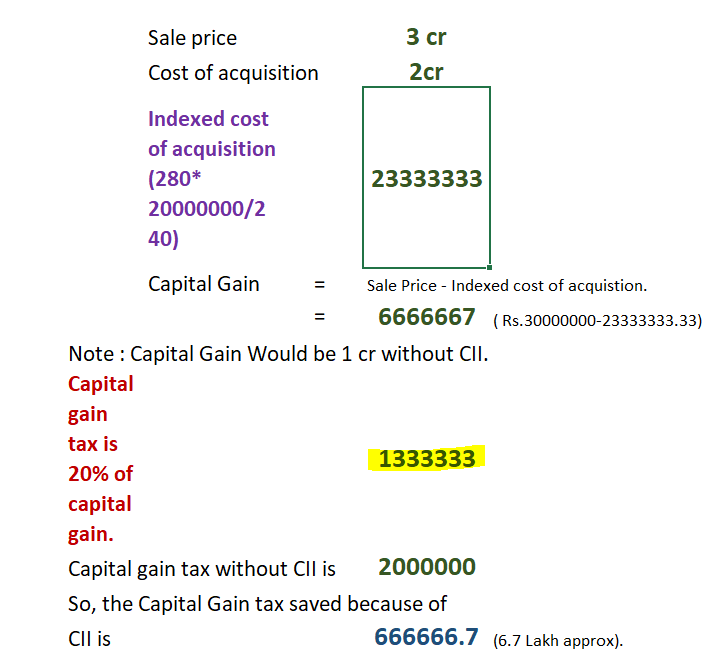

Let’s assume that You have bought a house in F.Y 2014-2015 with 2 cr.

In addition, Let’s assume that you sold this house in F.Y 2018-2019 for Rs.3 cr.

Now, Let’s calculate the LTCG after considering CII…

I think this article helped you in understanding the concept of the “Cost Inflation Index” in calculating Capital Gain Tax.

The source for the CII table is incometaxindia.gov.in.